Pros and Cons of Term Life Insurance

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

Dani Best

Licensed Insurance Producer

Dani Best has been a licensed insurance producer for nearly 10 years. Dani began her insurance career in a sales role with State Farm in 2014. During her time in sales, she graduated with her Bachelors in Psychology from Capella University and is currently earning her Masters in Marriage and Family Therapy. Since 2014, Dani has held and maintains licenses in Life, Disability, Property, and Casualt...

Licensed Insurance Producer

UPDATED: Jan 8, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider. Our life insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance related. We update our site regularly, and all content is reviewed by life insurance experts.

UPDATED: Jan 8, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider. Our life insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

With so many controversies concerning buying term life insurance, I wanted to present a few ideas for you to ponder and decide for yourself. Some are saying term life is a waste of money while others argue you should buy term and invest the difference.

I believe that there is no one policy that will fit every individual. We all have different needs, incomes, family sizes, and health histories to consider when acquiring a life insurance policy. To help work it out, let’s look at the advantages and disadvantages of term life insurance.

Related: How do I find the cheapest term life insurance rates (10 secrets)?

What Is Term Life Insurance?

As the name implies, term life insurance provides coverage for a specific time frame and pays a benefit only if you die suddenly during that particular term. Your beneficiaries will receive a set payment (known as the death benefit) as described in your policy.

Term periods typically range from 5 to 30 years with 20 years being the most popular term.

This type of insurance can also be referred to as “pure life insurance” since it has no savings component or any other added benefits. In short, it provides a guaranteed death benefit for a given period.

Compare Quotes From Top Companies and Save

What Happens When the Term Is Over?

When your term life insurance expires, you have 4 choices:

- Drop the policy – You no longer need it; you bought it 30 years ago, your house is paid off, the kids are married now and are not depending on your income anymore, and you saved enough money to support your wife or your final expense if needed. You should rejoice that you never needed to use it and you are still alive. It provided the certainty you needed for your heirs should something have happened to you.

- Extend your coverage – Most term life insurance doesn’t really expire at the end of your term. Most policies expire when the insured reaches 95 years old. You may continue with your current policy without taking an exam or proving insurability; however, it will be significantly more expensive, and the rate will increase every year as you age. It will renew on an annual basis. Some families are opting for that choice because they may need the coverage for 2–3 years (the insured has a terminal illness) so that they can collect the death benefit; however, most individuals do not opt for that choice. If you are healthy and need a policy, just get a new term or a final expense policy.

- Convert your policy – Most life insurance policies offer this choice. You may convert your policy into a Whole Life or Universal Life, though this will highly depend on if they are offering that product when your term expires. Keep in mind that this must be done before your term is over and typically before the age of 70. Just like extending your coverage, you don’t need to go through an exam or prove insurability. This is a good choice for people who still need life insurance but aren’t in the best of health, so either buying a new policy at a later age will cost too much or they could not be accepted.

- Buy a new term policy – For some, this may be the best choice. If you are still relatively healthy under the age of 60 years and don’t want to pay for a whole life policy, this will be the best choice for you. You can also get a no-exam policy if you choose this route, but keep in mind that you will pay more for that, and the max death benefit is usually $500,000.

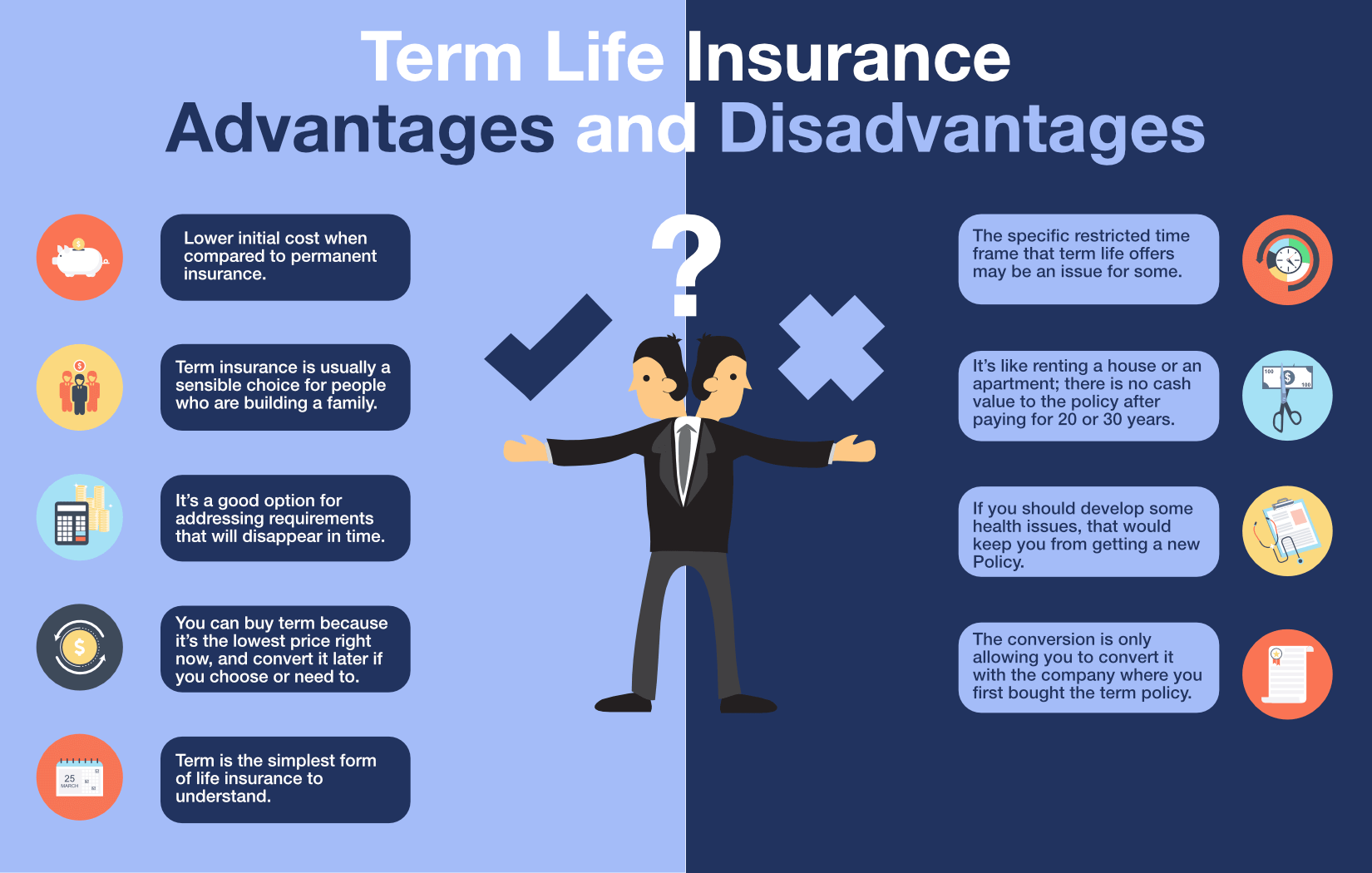

Advantages of Term Life Insurance

- One of the primary benefits of term insurance is its lower initial cost when compared to permanent insurance. The reason it’s cheaper is that, with a term policy, you’re typically just paying for the death benefit, the payment your beneficiaries will receive if you pass away during the term of the policy. With most permanent policies, your rates help fund the death benefit and can build up cash value.

- Term insurance is usually a sensible choice for people who are building a family, especially if they’re on a tight budget since it allows them to purchase higher levels of coverage when the need for protection is often greatest.

- It’s a good option for addressing requirements that will disappear in time. As an example, if paying for school is a significant financial concern, but you’re confident that you won’t require insurance coverage after the children graduate, then it might make sense to purchase term coverage that’ll get you through the school years. If you are healthy and looking for a fast underwriting decision, you may want to apply for a no-exam term policy.

- Since most term life policies offer the conversion benefit, it may appeal to you to buy term because it’s the lowest price right now, and you can convert it later if you choose or need to. So you aren’t really committing to any long-term policy such as whole life, but you keep the doors open for future needs.

- Term coverage is the simplest form of life insurance to understand. We all value something that is simple to understand. For instance, if you bought a 30-year policy when you were 30 years old, you should know it will expire at the age of 60.

Disadvantages of Term Life Insurance

- The specific restricted time frame that term life offers may be an issue for some. You can buy a $500,000 30-year term policy if you are in your 30s, but, if you wait to buy it when you 65 years old, you may get a 20-year policy. The term length is highly related to your current age at the time of the application.

- It’s like renting a house or an apartment; there is no cash value to the policy after paying for 20 or 30 years. Many will argue that they can save or invest for themselves and are happy to get rid of it after 30 years.

- If you should develop some health issues that would keep you from getting new insurance, you will be stuck with the high premiums to pay at the end of the term should you decide to keep it.

- The conversion built into many term plans is only allowing you to convert it with the company where you first bought the term policy. So, if you develop any health history, you are at the mercy of the product and services of the same company. If they don’t have a good permanent product, this is your only choice. It may have been the best term product 30 years ago, but now, at the age of 60, they only offer GUL as a permanent product, and this is your only choice.

Compare Quotes From Top Companies and Save

What Can Term Life Insurance Be Used For?

- Ensure your children are left with funds to help pay for school.

- Provide required protection as per a divorce agreement.

- Help your family take care of your final expenses and medical bills.

- Leave your family with sufficient funds to pay off debts such as a mortgage.

- Can be used by businesses for key person insurance or buy/sell agreements.

- Provide short-term insurance coverage if you’re between jobs.

- Replace your income if you are to pass away unexpectedly.

Case Studies: Pros and Cons of Term Life Insurance

Case Study 1: Michael’s Growing Family

Michael is a 32-year-old married individual with two young children. He wants to ensure his family’s financial security in the event of his premature death. After careful consideration, Michael decides to purchase a 25-year term life insurance policy. Here’s how he assesses the advantages and disadvantages:

Michael recognizes the lower premiums compared to permanent life insurance options, allowing him to allocate more funds towards other financial goals. He finds the sufficient coverage provided by the policy valuable in replacing his income and supporting his family’s living expenses, mortgage payments, and children’s education costs.

The flexibility to choose a term that aligns with his long-term financial obligations is also appealing. Michael acknowledges that the term life insurance policy has no cash value accumulation or investment component.

He understands that the coverage ends after the policy term, leaving his family without lifelong protection if he outlives the term. He is aware that premiums may increase significantly if he decides to renew the policy or purchase a new one after the initial term.

Case Study 2: Lisa’s Business Loan Protection

Lisa is a 45-year-old small business owner who recently obtained a loan to expand her company’s operations. She wants to ensure that her business debts would be covered if something were to happen to her. Lisa chooses a 15-year term life insurance policy and evaluates the pros and cons:

Lisa appreciates the affordability of the premiums, which fit within her business budget. She recognizes the sufficient coverage provided by the policy, ensuring that her business loan would be paid off and her company’s financial stability protected in case of her untimely death.

The flexibility to reassess coverage needs after the policy term ends aligns with her business’s financial situation. Lisa acknowledges that the term life insurance policy has no cash value growth or savings component.

She understands that the coverage duration is limited, which may not align with her long-term business goals. She is aware that premiums may increase if she wants to extend the coverage or obtain a new policy after the initial term.

Case Study 3: James’ Mortgage Protection

James is a 38-year-old homeowner who recently purchased a house with a substantial mortgage. He wants to ensure that his loved ones would be financially secure if he were to pass away unexpectedly. James decides on a 20-year term life insurance policy and weighs the advantages and disadvantages:

James recognizes the lower premiums compared to permanent life insurance options, allowing him to allocate more funds towards mortgage payments or other financial goals. He appreciates the adequate coverage provided by the policy, ensuring that the mortgage balance would be paid off and his family would have financial stability in case of his untimely death.

The flexibility to reassess coverage needs after the policy term ends aligns with his family’s changing financial situation. James understands that the term life insurance policy has no cash value accumulation or investment component.

He acknowledges that the coverage ends after the policy term, leaving his family without lifelong protection if he outlives the term and still has financial obligations. He is aware that premiums may increase if he decides to extend the coverage or purchase a new policy after the initial term.

Last Word

Term life insurance is probably the most popular form of protection because of its lowest cost. Whether you buy whole life or term insurance, you will still need to be in great health to get the lowest rates.

So, it’s not necessarily the type of plan that you buy but the risk you pose to the insurance carrier that ultimately determines your rates. You can go ahead and run term life insurance rates on this page.

Frequently Asked Questions

What is term life insurance?

Term life insurance provides coverage for a specific period and pays a death benefit if you die during that time. It’s a straightforward policy with no savings component.

What happens when the term is over?

When the term of your policy ends, you have four choices: renew, convert to permanent insurance, let it lapse, or buy a new policy.

What are the advantages of term life insurance?

Advantages of term life insurance include lower premiums, flexibility in choosing the term, simplicity in understanding the policy, and temporary coverage for specific needs.

What are the disadvantages of term life insurance?

Disadvantages of term life insurance include no cash value or investment component, coverage limitations if you outlive the term, potential for increasing premiums, and no lifelong coverage.

What can term life insurance be used for?

Term life insurance can be used for replacing lost income, paying off debts, covering childcare and education expenses, and providing business protection.

Compare Quotes From Top Companies and Save

Dani Best

Licensed Insurance Producer

Dani Best has been a licensed insurance producer for nearly 10 years. Dani began her insurance career in a sales role with State Farm in 2014. During her time in sales, she graduated with her Bachelors in Psychology from Capella University and is currently earning her Masters in Marriage and Family Therapy. Since 2014, Dani has held and maintains licenses in Life, Disability, Property, and Casualt...

Licensed Insurance Producer

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance related. We update our site regularly, and all content is reviewed by life insurance experts.